In line with Wikipedia’s narration, An internship is a period of work experience offered by an organization for a limited period of time. It is an opportunity that employers offer to students interested in gaining work experience in particular industries. With this piece of work I have put together, learn more about what internships are and why students like myself benefited from them. This is a practical work I submitted to my University, University of Professional Studies — Accra (UPSA), an accredited member of the Council for Business Schools and Programmes (ACBSP) in America. I did this work in 2017, a year before I will be graduating. Learn as much and have a feel about the 3 months internship experience. When you are done with yours, let other people also benefit from your experience as I have done. One day, someone you would never meet in this life, will be glad to read your piece of work and benefit as much.

ACKNOWLEDGEMENT

As my academics and internship experience are success, I express my deepest appreciation to all those who provided me the opportunity and guidance. First and foremost, I thank the almighty Lord for giving me Life. I cannot wish for anything more from Him. A special gratitude I give to the Director of Finance, Mr. Emmanuel Dupon Anson, of Solutions Technologies Limited, who gave me the chance of doing internship with this esteem company. I say thank you very much Director. To my boss and supervisor, Mr. Enock Wiafe, your contribution in stimulating suggestions and encouragement is forever going to guide me in my accounting career path, thank you sir. I would also like to acknowledge with much appreciation the important role of the staff of Solutions Technologies Ghana, especially, Agnes Danso, who in spite of her duties, got time to listen, guide and keep me on the correct path. To Beatrice and Eugene Addo, my internal audit work could not have been completed without your time in providing the needed documents. I say thank you.

Furthermore, distinguished appreciation also goes to the management of University of Professional Studies most especially the Vice Chancellor, Professor Abednego Feehi Okoe Amartey. The Dean, Dr. Raymond Dziwornu and the Head of Accounting Department (HOD), Dr. Mrs. Helena Ahulu and all others involved in making internship part of the academic assessment to enable students gain the aspiring work experience before graduating. Many thanks also goes to The Director, Public Affairs, Mr JSK Agbenyo and the entire Industrial Relations Office for their unending assistance. I can never forget to mention my Uncle and guardian, Mr. Solomon Anomah Larbi, if it hadn’t been him, my education would have ended at the lower level, primary three (3). God bless you daddy.

EXECUTIVE SUMMARY

This is an internship report, undertaken by Mr. Akonnor Owusu Larbi (10020849) at Solutions Technologies Company Limited — Madina. The intern started his internship from 19th June to 18th August, 2017. In fulfillment of the requirement of the Degree, Professional and Tertiary Diploma programs pursued at the University of Professional Studies, Accra, it is mandatory for level 300 students to have a minimum of two (2) months practical industrial experience in their respective fields of training and organization of their choice. An Industrial attachment is essential requirement for awarding of Bachelor Degree Certificate in the University of Professional Studies, Accra (UPSA).

The purposes of the internship is to prepare the student to serve the needs of industry and commerce more effectively upon graduation. This included providing real life experience and exposure, thus gaining first-hand exposure of working in the real world, granting the opportunity to learn more about the intern self-potentials and abilities, getting connected and developing professional network, preventing CV from going to trash during job application and transition to full-time job position. Internship allows students to harness the skill, knowledge and theoretical practice they learnt in the University and enabling them to transform theory into practical real life situations. The intern’s time with Solutions Technologies Limited has really illuminated his knowledge and understanding of practical experience of the theories being taught between the walls of the University lecture halls and in the corporate environment.

Table of Contents

ACKNOWLEDGEMENT. 2

EXECUTIVE SUMMARY. 3

1.0 INTRODUCTION.. 4

1.1Background Of The Report 4

1.2 Terms of Reference. 5

1.3 Purpose of Attachment/Expected Output. 6

1.4.0 Profile of the Organization. 7

1.4.1 Background. 7

1.4.2Mission. 7

1.4.3Objectives. 8

2.0 FIELD OF EXPERIENCE. 9

2.1 Duties and schedules. 10

2.2 Contributions of Student to the Organization. 12

2.3 Application of Theories to Real Life Situation. 13

3.0 LESSONS LEARNT. 15

4.0 CHALLENGES. 16

5.0 CONCLUSION.. 17

6.0RECOMMENDATIONS. 18

7.0 REFERENCES. 19

8. 0 APPENDIX 1. 19

1.0 INTRODUCTION

1.1Background of the Report

As part of my four (4) years Bachelor’s Degree studies in Accounting per the requirement of the University of Professional Studies, Accra, it is mandatory for Level 300 students going to level 400 the next academic year to perform an internship. Students being degree or diploma are to embark on this internship for minimum of two months to enable them obtain practical industrial experience in the field of study and also to abreast themselves of the business environment. The report is written at the end of the internship by the student to the institute which form part in the awarding of the degree certificate. The intern did a nine (9)-week internship (19th June to 18th August 2017) at Solutions Technologies Ghana Limited that was established in April 2010 as a company limited by liability. Currently there are five (5) departments at the company (Finance Department, Administration Department, Marketing Department, Sales Department and Technical Department) and each one of them has been projected to comprise of several divisions. The intern was assigned to the Finance Departments. The main duty was to assist the Accountant with implementation of the goals of the department, which included various tasks depending on the daily activities like checking of petty cash, payment vouchers, Bank Lodgment, Reconciliation, Input of records in tally software and preparing of monthly financial reports. However, the foremost area the intern specialized was Internal Audit. The intern was the first person ever to be given this duty ever since the company was established. The intern started the internship by reading the International Financial and Reporting Standards (IFRS) and the International Accounting standards (IAS) in Financial Reporting. The Finance Director, Mr. Emmanuel Dupon Anson, urged to pay much attention to IAS 11, Construction contracts, since the company get most of its revenue from Consultation relating to Telecom contracts in Zambia, DR. Congo, Cameroon and few others to mention.

An internship is an extensive program through which an intern can learn the practical aspects of what is taught between the four walls of the University lecture halls. The internship help students to learn, know and understand what actually happen on the field as compared to what they have studied in the school. This is a report on the purpose of carrying out the internship, the profile of the chosen organization of the intern, duties and schedules performed in the organization, the contributions of the intern to the organization, application of theories to real –life situations, various lessons learnt by the intern, challenges encountered, conclusions drawn and recommendations made by the intern.

1.2 Terms of Reference

In accordance to the Industrial Relations Office of the University of Professional Studies, Accra (UPSA), as part of it academic policy for every student, at the end of level 300 (6th semester), the university place students with various business organizations for a minimum period of two months to enable them obtain practical industrial experience in their respective field of training and also to submit a written report after the internship. As stated in the Undergraduate Students Handbook 2014/2016, the internship with it course code BCPC 401 is a three (3) credit hours course. The internship report entails areas such as purpose of attachment, profile of the organization or institution, contribution of student to organization, application of theories to real life situation, challenges faced and lessons learnt from the organization as well as recommendations from students.

1.3 Purpose of Attachment/Expected Output

By the requirements of the University Of Professional Studies, Accra (UPSA) to the award of degree and diploma certificates, it is a pre-condition that every student upon moving to the final year undertake an industrial attachment with a selected organization of their choice. The internship provides students the opportunity to gather some work experience relevant to their studies and their professional work field. It helps the student to learn discipline and principles of working ethics.

The following are the purposes of the internship:

Ø An internship provides a real life experience and exposure. It enables the intern to gain first-hand exposure of working in the real life which is remarkably valuable towards the intern’s career.

Ø It allows the student to harness the skill, knowledge and theoretical practice been taught in the university. To provide the students with an opportunity to apply the knowledge in real work situation thereby closing the gap between academic work and the actual practice.

Ø Internship teaches young professionals about specific industries and companies they are interested in, projects their self-potentials, abilities and shortcoming.

Ø Get connected, develop professional network and transition to full-time position.

1.4.0 Profile of the Organization

1.4.1 Background

Solutions Technologies Limited (Solutec) is a licensed business operating under the Companies Code of the Republic of Ghana offering IT Solutions and Consultancy with registration number CS423302014. The company’s Head Office is situated at 4 Naa Adjetey Sowah Street, behind Barclays Bank, Madina — Accra. It has a branch located at 52 Castle Road, Behind HFC Bank, Adabraka- Accra. The company brands itself; Everything ICT.

Founded in April 2010, Solutions Technologies Limited is proud to be a one stop shop for telecommunication and networking solutions in Ghana. Solutec provides not only excellent services, but a complete array of robust telecommunication accessories nationwide with other complimentary set of ICT Solutions. The company has a significant synergies with many African, European and US institutions. There are five (5) departments at the company which is made up of Finance Department, Administration Department, Marketing Department, Sales Department and Technical Department.

1.4.2Mission

The mission statement of Solutions Technologies Ghana is to be a world class ICT Solution provider with innovative and responsive services that support customer needs.

1.4.3Objectives

ü To be a leader in connectivity

ü Valuing customers and constantly building key relationships.

1.4.4Product Goods and Services

Solutions Technologies Limited offer the following services;

Consultancy & Tech Support: Solutions Technologies Ghana provides consultancy and technology support in project management for corporate bodies on contract basis. The company focuses on advising organizations on how best to use information technology in achieving their business objectives. In addition to providing advice, Solutec often estimate, manage, implement, deploy and administer IT Systems on behalf of their client organizations.

Sales: The Adabraka branch is concerned with sales of IT products, including Ubiquity, Mikrotik, TP –Link, D- Link and Yeaster.

Renewable Energy Solutions: The Company is also into the sales and installation of solar panels for individuals and corporate bodies.

Security Solutions: This includes services in CCTV Cameras, Access control, Car tracking, Time & Attendance.

Telecommunication: This has to do with providing service relating to Wireless LAN, VoIP and Satellite Dish. VoIP means Voice over Internet Protocol. This is the transmission of voice and multimedia content over Internet Protocol (IP) networks, Enterprise Local Area Networks or Wide Area Networks.

Solutec Academy; Training & Courses including Hardware and Networking, Cisco, Information Systems, System Analysis and Design, Certificate and Diploma in Information Technology and Tally Software Certificate.

Web Solutions: Solutec Ghana is also involved with web design and web hosting. The company offers industry experts. They create for their clients the best responsive website to date with the latest trends and technologies.

2.0 FIELD OF EXPERIENCE

During the internship period, the intern was assigned to the Finance Departments at the Head Office of Solutions Technologies Ghana. The Finance Department is responsible for the corporate financial accounting function and oversight of the financial accounting processes of the company. This includes: ensuring financial statements are completed timely and accurately in compliance with GAAP, and that the company accounting records contain the information necessary to meet reporting requirement to internal management, for tax compliance and reporting of financial results to management. The main duty was to assist the Accountant with implementation of the goals of the department, which included various tasks depending on the daily activities like checking of petty cash, payment vouchers, Bank Lodgment, Reconciliation, Input of records in tally software and preparing of monthly financial reports. However, the foremost area the intern specialized was Internal Audit. The intern was the first person ever to be given this duty since the company was established. Audit performed were external audits and risk assessment had never been done.

2.1 Duties and schedules

The intern was assigned to the following duties and responsibilities

ü Filing of Petty Cash Request Forms

ü Bank Statements Reconciliation

ü Handled Accounts Receivables

ü Planning and Providing Internal Controls on Cash Handling and Warehousing

ü Planning the Budget for a new branch in Kumasi

ü Planning and Performing of Internal Audit

Filing of Petty Cash Request Forms

The intern’s first duty was filing of petty cash request forms. The intern got to understand that filling is the term used for the arrangement of documents in order to be able to find them easily and quickly. The task given to the intern was to be done for every day. The intern was also to ensure that petty cash above GH¢200 had supporting documents attached. Filing system is the central record-keeping system for Solutions Technologies Ghana. It helps the company to be organized, systematic, efficient and transparent. It also helps all people who want access to the information do so more easily. Clip folders are used to hold petty cash request forms tightly so that they do not fall.

Bank Statements Reconciliation

Another task assigned to the intern was reconciling the company’s bank statements. When the company receives its bank statement, the company verifies that the amounts on the bank statement are consistent or compatible with the amounts in the company’s cash account in its general ledger and that of the general ledger is also consistent with the bank statement. This process of confirming the amounts is referred to as reconciling of Bank Statement. The intern held this duty anytime it had to be performed. After the reconciliation, the intern reported to his supervisor, the Accountant, Mr. Enoch Wiafe.

Handled Accounts Receivables

One other duty the intern was responsible for was the handling of accounts receivables. Improper managed accounts receivable is one of the most common causes of cash flow shortages. Since the company has clients from Europe, US and other African Countries, some of the accounts receivables were in US Dollars. The intern had the duty of confirming payments made by clients according to account records and payments client claim they have made. This sometimes gets a little bit challenging.

Planning and Providing Internal Controls on Cash Handling and Warehousing

Before the intern was assigned to perform an internal audit for the company’s branch at Adabraka- Accra, he was made to plan and provide internal control measures on Cash Handling and Warehousing. The intern designed a checklist to track and monitor internal controls in the company and the areas that needs management attention. These internal controls enlightened the intern’s knowledge on Risk Assessment that many organizations faces.

Planning the Budget for a new branch in Kumasi

Solutions Technologies Ghana has projected opening a new branch in Kumasi. The new branch will be concerned with sales of IT products. The marketing department had already gone to the region to do their market research and survey. The intern was assign with the planning of a detailed budget. A budget is an estimate of income and expenditure for a set period of time. This detailed budget included, salaries, advertising, rent, office expenses, cost of products, shipping charges and profit projection, for the Kumasi Branch.

Planning and Performing of Internal Audit

The foremost area the intern specialized was Internal Audit. The intern was given the right to conduct an official financial inspection of the company’s branch at Adabraka. This includes organizing large amount of files to make sure they were in order before the preparation for internal audit. Internal Audit is concerned with evaluating and improving the effectiveness of risk management, control and governance processes in an organization. The intern was given a deadline to submit an audit report to management. The Audit was conducted for two (2) accounting periods, January to December 2016 and January to June 2017. The audit particularly covered Revenue and Expenses. The intern was made to generate a report to the Finance Director about the invoices, sales, payment vouchers, petty cash and bank lodgment audited. The audit was to give a reasonable assurance about whether the financial statements are free from material misstatement, either caused by error or fraud.

2.2 Contributions of Student to the Organization

Planning and Providing Internal Controls on Cash Handling and Warehousing. The intern designed a checklist to track and monitor internal controls in the company and the areas that needs management’s attention. This task will assist management in tackling the hidden risk the company has possibility of facing in the near future.

Planning and budgeting for a new branch of the company at Kumasi. The budget the intern drew was applauded by the accountant. It gave a detailed analysis of the cost involved and revenue projections. This project will resume latest by March 2017.

The intern also wrote a proposal to the accountant which involved a strategic sales generation procedure. The proposal aimed to forge a strategic sales generation presentation to leverage the customer base for the company’s distinct services.

Conducting of Internal Auditing and providing report. The intern solely conducted an internal audit to establish the areas of risk regarding Revenue and Expenses of the company. He established controls to address these risks and made recommendations where weakness or inefficiencies are observed.

The interns understanding of responsibilities to a specific job, as well as willingness to get things done, performing different activities with limited time and take responsibility for his actions were exceptional.

2.3 Application of Theories to Real Life Situation

The internship provided the opportunity for the intern to understand practically how theories were applied in the business world. The following are the application of theories to real life situations at Solutions Technologies:

Communication Theory

Communication is the exchanging of information by speaking, writing or using some other medium. It gives an explanation of the basic process individuals go through in order to gain information and knowledge about other people. The intern had learnt communication skills with course code BGEC 101 and Business Communication with course code BGEC 103, this gave the intern exceptional interpersonal communication skills that made him understand how to approach, talk and respond to different people of different backgrounds at the work place. The intern found out that being able to apply communication theories to real life scenarios made him a better communicator.

Cognitive Resource Theory

Cognitive Resource Theory is a topic under BCPC 207 which is Principles of leadership. This course was taken in level 200 semester 1 by the intern. The theory explains how intelligence and experience relate to stress. Intelligence is the main factor in low-stress situations, whilst experience counts for more during high-stress moments. The intern inculcated this theory in the performance of most duties.

Esprit de Corps

Esprit de corps is the feeling of camaraderie (solidarity) that exist among members of a group or an organization. The intern had been at the company for the first few weeks but he was already bound to the staff by a strong esprit de corps. There was unity among the staffs and this stretched to the intern. The intern also realized that the staff of the company worked together as a team to achieve the goals of the company, the output of one department served as the input for another department. A practical example is, the marketing department gets a contract for the company, administration department have the meeting with the client and agree on the terms and conditions of the contract and finally the technical department execute the project. Before and after the completion of the project, the accounts department computes all charges receivables.

Theory of Motivation

Apart from the payment of basic salaries to staff, there were also provisions designed to improve conditions of workers at Solutions Technologies Limited. One good example is the surprise celebration of staffs’ birthdays by the Finance Director. This was done to make subordinates feel like they are in a family and encourage them to achieve a certain goal or level of performance.

3.0 LESSONS LEARNT

During the internship the intern learn the following lessons:

ü The intern now has good understanding of Generally Accepted Accounting Principles (GAAP)

ü Strong PC Skills utilizing Microsoft Excel, Word, Outlook and Tally Software.

ü Ability to work with different people (team work) in achieving departmental as well as organizational goal.

ü Excellent verbal and written communication skills.

ü Strong organizational and time management skills.

ü Planning and Preparing of Audit.

ü Insight on Governance, Risk Assessment and Compliance

ü Learn the culture of the IT industry.

4.0 CHALLENGES

The major challenge the intern faced was a new Lifestyle. The internship gave a new lifestyle to the intern. It made the intern woke up very early in the morning with the alarm clock at 5:30 am, latest by 6 am to get ready for work. The intern sat for nine (9) to ten (10) good hours in a day typing and preparing either reports or doing an online research about a particular task. Sometimes the intern could close as late as 8:30 pm. The new life was quite jarring but productive. The hours and the new living situation clearly made socializing more difficult than before. This challenge later became normal and part of the intern’s daily life activities as the days moved on.

The intern also encountered financial difficulties including food and transportation. Financial problems and challenges happen to everyone at some point, and the stress and worry can get to anyone. However, realizing that there is an important task ahead to complete kept the intern going. It is not easy to overcome it but with perseverance, determination and dedication, the task ahead was achieved.

Conducting audit with no audit experience and assistance. To add, the intern was assigned to conduct an internal audit of a branch of the company at Adabraka individually. This was a major task for the intern as he had no prior audit experience. For the beginning, the intern found himself wanting but as time went on, the intern gained practical experience on the job. The audit became less difficult because the intern had completed a University course in Auditing just before vacation. The intern therefore applied the theoretical aspect of the auditing learnt at school on the field.

All these challenges has helped the intern to gain valuable work experience and real life exposure. It also allowed the student to harness the skill, knowledge and theoretical practice been taught in the university.

5.0 CONCLUSION

The placement program was exclusively of boundless achievement to the intern. The internship program aided the intern to have an in-depth knowledge about the practical problem solving in the corporate world. The intern has been enlightened on the application of theories in real life situations. Solutions Technologies Limited has offered the intern opportunities to learn and develop himself in many areas. This internship has prepared the student to be ready to serve the needs of industry and commerce more effectively upon graduation. This included providing real life experience and exposure, thus gaining first-hand exposure of working in the real world, granting the opportunity to learn more about the intern self-potentials and abilities, getting connected and developing professional network. I gained a lot of experience, especially in the conducting of internal audit. Before the placement took place, my ideas did not match the experiences I have gained during my internship. This internship was definitely an introduction to the actual work field for me. I have learned to work in a business organization and apply my knowledge into practice. Deepest gratitude I give to the management of Solutions Technologies Limited, most especially the Finance Director, Mr. Emmanuel Dupon Anson, the accountant, Mr. Enoch Wiafe and all the staff of the company for the great opportunity given to me for their careful and exquisite guidance which were extremely valuable for my study both theoretically and practically. I perceive this opportunity as a big breakthrough in my career development.

6.0RECOMMENDATIONS

To Management and Staff of Solutions Technologies Limited;

Solutions Technologies Limited should try and develop some control measures in relating to both the Madina and Adabraka inventory room. Especially with Madina, a check sheet should be provided and be with the secretary. Anytime someone wants to go there for any purpose, the person has to sign and write the purpose and time he came for the inventory room keys. This will help to hold persons that went there responsible for any missing stock.

Also, the malfunctioning POS machine at the Adabraka branch should be a major concern to management. The machine should be repaired or replaced as soon as possible.

Finally, Solutions Technologies should develop a customer support committee. The committee will see to it that customers are frequently called and visited to observe services that were provided to them by the company. The company should not wait for customers to call and complain about faulty issues before they set off. This when done, will boost customer confidentiality in the company and build a strong and lasting relationship.

To UPSA Industrial Relation

The industrial relation office and the different departments should connect with cooperate bodies for internship placement to shun the struggles and strains students go through before securing places for their attachment.

7.0 REFERENCES

University of Professional Studies Students’ Handbook.

Guideline for Internship Report University of Professional Studies Accra (UPSA)

8. 0 APPENDIX 1.

INTERNSHIP FRAMEWORK

Objectives

The internship program as a three (3) credit hour course with course code BCPC 410 is to provide a real life experience and exposure to the student. To enable the intern gain first-hand exposure of working in the real life which is remarkably valuable towards the intern’s career.

APPENDIX 2

STAFF

I would like to thank all staff that provided assistance during the course of this internship, and in particular:

Ø Finance Director

Ø Accountant

Ø Secretary

Ø Sales officers

The Maxims of Equity

Maxims of equity are principles developed by the English Court of Chancery and other courts who have administered equity jurisdiction, including the law of trusts. They were often expressed in Latin but are translated into English.

The twelve equitable maxims are:

1. Equity Will Not Suffer A Wrong To Be Without A Remedy

2. Equity Follows the Law

3. He Who Seeks Equity Must Do Equity

4. He Who Comes Into Equity Must Come With Clean Hands

5. Delay Defeats Equities

6. Equality Is Equity

7. Equity Looks to the Intent Rather Than the Form

8. Equity Looks On That As Done Which Ought To Be Done

9. Equity Imputes an Intention to Fulfill an Obligation

10. Where The Equities Are Equal, The First In Time Shall Prevail.

11. Where There Is Equal Equity, The Law Shall Prevail.

12. Equity Acts In Personam.

1. EQUITY WILL NOT SUFFER A WRONG TO BE WITHOUT A REMEDY

Meaning

Where there is a right there is a remedy. This idea is expressed in the Latin Maxim ubi jus ibi remedium. It means that no wrong should go unredressed if it is capable of being remedied by courts. This maxim indicates the width of the scope and the basis of on which the structure of equity rests. This maxim imports that where the common law confers a right, it gives also a remedy or right of action for interference with or infringement of that right.

Application and cases

In Ashby v. White, wherein a qualified voter was not allowed to vote and who therefore sued the returning officer, it was held that if the law gives a man a right, he must have a means to maintain it, and a remedy, if he is injured in the enjoyment of it.

In cases where some document was with the defendant and it was necessary for the plaintiff to obtain its discovery or production, a recourse to the Chancery Courts had to be made for the Common Law becoming ‘wrongs without remedies’.

Limitation

a) If there is a breach of a moral right only.

b) If the right and remedy both were in within the jurisdiction of the Common Law Courts.

c) Where due to his own negligence a party either destroyed or allowed to be destroyed, the evidence in his own favour or waived his right to an equitable remedy.

Recognition

i) The Trust Act

ii) Section 9 of CPC- entitles a civil court to entertain all kinds of suits unless they are prohibited.

iii) The Specific Relief Act- provides for equitable remedies like specific performance of contracts, injunction, and declaratory suits.

2. EQUITY FOLLOWS THE LAW

Meaning

The maxim indicates the discipline which the Chancery Courts observed while administering justice according to conscience. As has been observed by Jekyll. M.R: ‘The discretion of the court is governed by the rules of law and equity, which are not to oppose, but each, in turn, to be subservient to the other.” Maitland said, “Thus equity came not to destroy the law but to fulfill it, to supplement it, to explain it.” The goal of equity and law is the same, but due to their nature and due to historic accident they chose different paths. Equity respected every word of law and every right at law but where the law was defective, in those instances, these Common Law rights were controlled by recognition of equitable Rights. Snell therefore explained this maxim in slightly different way: “Equity follows the law, but not slavishly, nor always.”

Application and cases

At common law, where a person died intestate who owned an estate in fee-simple, leaving sons and daughters, the eldest son was entitled to the whole of the land to the exclusion of his younger brothers and sisters. This was unfair, yet no relief was granted by Equity Courts. But in this case it was held that if the son had induced his father not to make a will by agreeing to divide the estate with his brothers and sisters, equity would have interfered and compelled him to carry out his promise, because it would have been against conscience to allow the son to keep the benefit of a legal estate which he obtained by reason of his promise. This decision was held in Stickland v. Aldridge.

Equity follows the law and even if by analogy law can be followed, it should be followed.

Limitation

i) Where a rule of law did not specifically and clearly apply

ii) Where even by analogy the rule of law did not apply

Recognition

Bangladesh has not recognized the well-known distinction between legal and equitable interests. Equity rules in Bangladesh, therefore, cannot override the specific provisions of law. As for example, every suit in Bangladesh has to be brought within the limitation period and no judge can create an exception to this or can prolong the time-limit or stop the rule from taking effect on principles of equity. Such a decision was held in Indian Appa Narsappa Magdum case.

3. HE WHO SEEKS EQUITY MUST DO EQUITY

Meaning

The maxim means that to obtain an equitable relief the plaintiff must himself be prepared to do ‘equity’, that is, a plaintiff must recognize and submit to the right of his adversary. Scriptures of Islam also inform us to be conscientious:

“Woe to those who stint the measure:

Who when they take by measure from others, exact the full;

But when they mete to them or weigh to them, minish…”

Application and cases

This maxim has application in the following doctrines-

i) Illegal loans

ii) Doctrine of Election

iii) Consolidation of mortgages

iv) Notice to redeem mortgage

v) Wife’s equity to settlement

vi) Equitable estoppel

vii) Restitution of benefits on cancellation of transaction

viii) Set-off

i) Illegal loans: In Lodge v. National Union Investment Co. Ltd., the facts were as follows. One B borrowed money from M by mortgaging certain securities to him. M was a unregistered money-lender. Under the Money-lenders’ Act, 1900, the contract was illegal and therefore void. B sued M for return of the securities. The court refused to make an order except upon the terms that B should repay the money which had been advanced to him.

ii) Doctrine of election: Where a donor A gives his own property to B and in the same instrument purports to give B’s property to C, B will be put to an election, either accept the benefit granted to him by the donor and give away his own property to C or retain his own property and refuse to accept the property of A on condition. But B cannot retain his property and at the same time take the property of A.

iii) Consolidation of mortgages: Where a person has become entitled to two mortgages from the same mortgagor, he may consolidate these mortgages and refuse to permit the mortgagee to exercise his equitable right to redeem one mortgage unless the other is redeemed. The right of consolidation now exists in England but after the enactment of the Law of Property Act, 1925, it can exist only by express reservation in one of the mortgage deeds.

iv) Notice to redeem mortgage: Notice to a mortgagor to redeem one’s mortgage is an equitable right of the mortgagor.

v) Wife’s equity to a settlement: There was a time when woman’s property was merged with that of her husband. She had no property of her own. Equity court imposed on the husband that he must make a reasonable provision for his wife and her children. But, now, Under the Law Reform (Married Women and Tortfeasors) Act, 1935, married women has full right on her property and it is not consolidated with her husband’s property.

vi) Equitable estoppel: A promissory estoppel arises where a party has expressly or impliedly, by conduct or by negligence, made a statement of fact, or so conducted himself, that another would reasonably understand that he made a promise thereon, then the party who made such promise has to carry out his promise.

vii) Restitution of benefits on cancellation of transaction: It is proper justice to return the benefits of a contract which was voidable, and, equity enforced this principles in cases where it granted relief of rescission of a contract. A party can not be allowed to take advantage of his own wrong.

viii) Set-off: Where there have been mutual credits, mutual debts or other natural dealings between the debtor and any creditor, the sum due from one party is to be set-off against any sum due from the other party, and only the balance of the account is to be claimed or paid on either side respectively.

Limitation

i) The demand for an equitable relief must arise from a suit that is pending.

ii) This maxim is applicable to a party who seeks an equitable relief.

Recognition

i) Under sec 19-A of the Contract Act, 1872 if a contract becomes voidable and the party who entered into the contract voids the contract, he has return the benefit of the contract.

ii) sec 35 of the Transfer of Property Act embodies the principle of election.

iii) Sec 51 and 54 of the Transfer of Property Act.

iv) In Order 8, Rule 6 of the CPC, the doctrine of Set-off is recognized.

4. HE WHO COMES INTO EQUITY MUST COME WITH CLEAN HANDS

Meaning

Equity demands fairness not only from the defendant but also from the plaintiff. It is therefore said that “he that hath committed an inequity, shall not have equity.” While applying this maxim the court believed that the behavior of the plaintiff was not against conscience before he came to the court.

Application and cases

In Highwaymen case, two robbers were partners in their own way. Due to a disagreement in shares one of them filed a bill against another for accounts of the profits of robbery. Courts of equity do grant relief in case of partnership but here was a case where the cause of action arose from an illegal occupation. So, the court refused to help them.

The working of this maxim could be seen while giving the relief of specific performance, injunction, rescission or cancellation.

Limitation

General or total conduct of the plaintiff is not to be considered. It will be seen whether he was of clean hands in the same suit he brought or not. Brandies J. in Loughran v. Loughran said that “Equity does not demand that its suitors shall have led blameless lives.”

Exception

i) If the transaction is a against public policy

ii) if the party repents for his conduct before his unjust plans are carried out.

Recognition

i) Section 23 of the Indian Trust Act- An infant can not setup a defence of the invalidity of the receipt given by him.

ii) Section 17, 18 and 20 of the Specific Relief Act, 1877- Plaintiff’s unfair conduct will disentitle him to an equitable relief of specific performance of the contract.

Distinction between maxim no. 3 and 4-

He who seeks equity must do equity

He who comes into equity must come with clean hands

i) It is applicable when both the plaintiff and the defendant have claims of equitable relief against each other.

i) It is applicable when the defendant has no separate claim to relief and the plaintiff’s conduct is unfair.

ii) It exposes the condition subsequent to the relief sought.

ii) It is a condition precedent to seeking equitable relief.

iii) It refers to the plaintiff’s conduct as the court thinks it ought to be, after he comes to the court.

iii) It refers to the plaitiff’s conduct before he approaches the court.

iv) The plaintiff has to mould his behavior according to the impositions by the court.

iv) If the plaintiff’s conduct is unfair, it would not entitle him to the relief sought.

v) The plaintiff has an option or a choice before him either to submit to the conditions put by the court, or to get out of the court.

v) The conduct of the plaintiff snatched his choice from him. His equitable right therefore neither be recognized nor enforced.

vi) This maxim looks to the future.

vi) This maxim looks at the past.

5. DELAY DEFEATS EQUITIES

Meaning

A Latin term in this regard is “Vigilantibus, non dormentibus, jura subvenient.” which means “Equity aids the vigilant and not the indolent”. So, if one sleeps on his rights, his rights will slip away from him. Legal claims are barred by statutes of limitation and equitable claims may be barred not only by limitation law but also by unreasonable delay, called laches.

Application and cases

To cases which are governed by statutes of limitation either expressly or by analogy the maxim will not apply. Such cases fall into three categories-

i) Those equitable claims to which the statute applies expressly.

ii) to which the statute applies by analogy.

iii) Equitable claims which are covered by ordinary rules of laches.

Doctrine of laches- Plaintiff’s unreasonable delay is a weapon of defence by the defendant against the plaintiff.

In a Bombay case, the plaintiff allowed his land to be occupied by the defendant and this was acquiesced by him even beyond the period of limitation. On a suit of the land it was decided that as the period of limitation to recover possession had expired, no relief could be granted. Also the case of Allcard v. Skinner is worth mentioning here.

Limitation

This maxim does not apply when-

i) where the law of limitation expressly applies

ii) where it applies by analogy, and

iii) where the law of limitation does not apply but the cases are governed by ordinary rules of laches.

Recognition

The English doctrine of delay and laches showing negligence in seeking relief in a court of equity can not be imported into the Bangladeshi law in view of Article 113 of the Limitation Act, 1908, which fixes a period of one year (previously three years) within which a suit for specific performance should be brought.

Section 51 of the Transfer of Property Act embodies this doctrine but with a difference.

6. EQUALITY IS EQUITY

Meaning

Plato defined that “If you cannot find any other, equality is the proper basis.” This maxim is also explained as “equity delighteth in equality”, which means that as far as possible equity would put the litigating parties on an equal level so far as their rights and responsibilities are concerned.

Justice Fry said, “When I say equality, I do not mean equality in its simplest form, but which has been sometimes called proportionate equity.”

Application and cases

Application of this maxim can be understood from the following:

i) Equity’s dislike for joint tenancy and presumption of tenancy-in-common

ii) Equal distribution of joint funds and joint purchases

iii) Contribution between co-trustees, co-sureties and co-contractors

iv) Ratable distribution of legacies

v) Marshalling of assets

7. EQUITY LOOKS TO THE INTENT RATHER THAN THE FORM

Meaning

Common law was very rigid and inflexible. It could not respond favourably to the demand of time. It regarded the form of a transaction to be more important than its substance. It looked to the very letter of the agreement and not the intention behind it. On the other hand, Equity looks to the spirit not to the letter, it looks to the intention of parties and not to the words.

Application and cases

In case of sale of land, if a party fails to complete it within the fixed for it, he is at Common Law, in breach of the contract, but equity does not take this rigid attitude. It allows a reasonable time to the party to complete it.

The application can be seen in the following instances-

i) Relief against penalties and forfeitures

ii) Relief in regard to precatory trust

iii) Relief in regard to mortgages, the doctrine of equity of redemption and the doctrine of clogs on redemptions

iv) Attitude in regard to statute of frauds.

i) Relief against penalties and forfeitures- Common Law courts insisted on the literal form of the contract that if the contract is breached, certain amount must be given as compensation, though the actual loss is not that much. Equity interpret the purpose and intent of the contract itself. The principal object of the contract is to perform it and not the compensation. The compensation is a subsidiary matter.

ii) Precatory trust- A trust is created with- (1) an intention on his part to create a trust thereby, (2) the purpose of the trust, (3) the beneficiary, and (4) the trust property. Where an author uses words such as ‘I hope’, ‘I request’ or ‘I recommend’ the first condition is missing. In cases where subsequent ingredients are found, in early days, it was held by the equity courts that he had the intention. This view is in use now but not as liberally as before.

iii) Relief in regard to mortgages- The mortgagor has a right to obtain his property back by payment of the debt and that is his right of redemption. The mortgagor’s right of redemption is guarded by courts and this has been expressed in a well-known legal maxim, “Once a mortgage, always a mortgage, and nothing but a mortgage”.

iv) Attitude in regard to statute of frauds-

Recognition

i) Sec 55 of the Contract Act- If time is the essence of the contract, and it is not performed within the stipulated time, the contract or part of it which is unperformed would be voidable. If time is not the essence, the contract will not be voidable but entitles the promisee to damages.

ii) Section 74 of the Contract Act- only a reasonable compensation can be claimed.

iii) Sec 114-A of the Transfer of Property Act- Forfeiture clauses in a lease.

8. EQUITY LOOKS ON THAT AS DONE WHICH OUGHT TO BE DONE

Meaning

If someone undertakes an obligation for the other, equity courts look on it as done and as producing the same results as if the obligation had been actually performed. Equity courts therefore look to the acts of the person bound by his conscience and interpret and construe them in such a way that they amount to what ought to be done.

Application and cases

If A makes T trustee leaving 50,000 Taka to purchase a land for the use of B. T does not purchase the land and by the time, B dies leaving all immovable property to X and all movable property to Y. Now, who should get the 50,000 Taka? Equity in such cases would definitely regard the purchase of land which ought to have been made as made. The money thus goes to X.

The working of this maxim can be seen-

i) the doctrine of conversion

ii) Executory contracts

iii) doctrine of part performance

i) Doctrine of conversion- In the case of Lachmere v. Lady Lachmere, money was taken as land. Doctrine of conversion can convert the money into immovable property and immovable property into money.

ii) Executory contracts-

(a) Assignment of future property: When an assignment of property was made for consideration equity treated it as a contract to assign. When the property came into existence in such a contract it was treated as a complete assignment. As a leading case on this point, Holroyd v. Marshall can be cited.

(b) Agreement for a transfer: In Walsh v. Lonsdale, it was decided that an agreement for lease could be treated as a lease in equity.

iii) Doctrine of part performance: Under the equitable doctrine of part performance contracts pertaining to land were allowed to be formed by oral evidence where one of the parties did acts of pats performance. Maddison v. Alderson is a leading case on this point.

Recognition

Many of the doctrines of English equity have taken statutory form in Bangladesh. Insofar as equitable assignments are concerned no equitable estate is recognized in Bangladesh. A transfer of future property for consideration operates as a contract to be performed in future.

i) The Transfer of Property Act- A Contracts to sell Sultanpur to B. While the contract is still in force, he sells Sultanpur to C, who has notice of the contract. B may enforce the contract against C to the same extent as against A.

ii) The Specific Relief Act- Section 12 relating to the specific performance of part of a contract also illustrates the application of the maxim.

iii) The Trust Act- Where a person acquires property with notice that another person has entered into an existing contract affecting that property, the former must hold the property for the benefit of the latter.

9. EQUITY IMPUTES AN INTENTION TO FULFILL AN OBLIGATION

Meaning

Equity considered and estimated acts of parties. Thus where a person is under an obligation to do a certain act, and he does some other act which is capable of being regarded as an act in fulfillment of his obligation. In other words a person is presumed to do what he is bound to do.

In Sowden v. Sowden, a husband covenanted with the trustee of his marriage settlement to pay to them £50,000 to be laid out by them in purchase of land in a particular area D. He, in fact, never paid the sum, but after marriage purchased the land at D in his own name, for £50,000. He died and could not bring the land into settlement. Equity courts construed that he purchased land to fulfill his obligation.

Application and cases

i) Doctrine of performance and satisfaction

ii) Ademption

iii) Doctrine of presumption of advancement

iv) Relief against defective execution of power of appointment.

i) Doctrine of performance and satisfaction- Sowden v. Sowden and Lachmere v. Lady Lachmere cases are examples of performance. Satisfaction is the donation of a thing with it is to be taken in extinguishment of some prior claim of donee. This maxim is helpful where the presumed intention of the testator is to be found out; where the intention is express the maxim has no application.

ii) Ademption- Ademption is a transfer of property which operates as a complete or pro tanto substitution for a gift previously made by the will of the donor.

e.g. X by his will leaves his daughter Y one-third of his residuary estate. Thereafter on Y’s marriage X gives Y 20,000 Taka. X dies. 20,000 Taka is an ademption -complete or proportionately to the gift of one-third share of the residuary estate of X.

iii) Presumption of advancement- When a purchase or transfer of property without consideration is made by a father or a person in loco parentis, to or in the name of a child, a presumption arises. And the presumption is that it was for the benefit of the child. Such presumption, is known as ‘advancement’. The doctrine applies to cases of parent and child, husband and wife, of mother and child and even to illegitimate child, but not to a man and his mistress.

iv) Relief against defective execution of power of appointment- A power is an authority vested in a person to deal with or dispose of property not his own. A power may be legal or equitable but after 1925 all powers of appointment are necessarily equitable.

e.g. A holds 50,000 Taka upon trust to divide among a certain class of persons. A has no option is this matter He is bound to carry out the trust. On his failing to do so, the court will see that the property is duly divided.

A defective execution will always be aided in equity under the circumstances mentioned, it being the duty of every man to pay his debts, and a husband or a father to provide for child.

Recognition

i) The Succession Act- Presumption against satisfaction is mentioned here. In Hasanali v. Popatal, a testator, who had a sum of Rs 9000 as deposit from his brother, gave to is brother a legacy of Rs 9000 and it was held that the brother was entitled to both, the legacy and his deposit. But as decided in Rajmanuar case where a will contained a clear indication that the legacy was meant as a satisfaction of the debt due to X, X could not claim both as the section explains.

ii) The Trust Act- Where a person contracts to buy property to be held on trust for certain beneficiaries and buys the property accordingly, he must hold the property for their benefit to the extent necessary to give effect to the contract. Equity thus imputes an intention to fulfill an obligation.

10. WHERE THE EQUITIES ARE EQUAL, THE FIRST IN TIME SHALL PREVAIL.

This maxim operates that where there are two or more competing equitable interests; when two equities are equal the original interest (i.e., the first in time) will succeed.

11. WHERE THERE IS EQUAL EQUITY, THE LAW SHALL PREVAIL.

Equity will provide no specific remedies where the parties are equal, or where neither has been wronged. The significance of this maxim is that applicants to the chancellors often did so because of the formal pleading of the law courts, and the lack of flexibility they offered to litigants. Law courts and legislature, as lawmakers, through the limits of the substantive law they had created, thus inculcated a certain status quo that affected private conduct, and private ordering of disputes. Equity, in theory, had the power to alter that status quo, ignoring the limits of legal relief, or legal defenses. But courts of equity were hesitant to do so. This maxim reflects the hesitancy to upset the legal status quo. If in such a case, the law created no cause of action, equity would provide no relief; if the law did provide relief, and then the applicant would be obligated to bring a legal, rather than equitable action. This maxim overlaps with the previously mentioned “equity follows the law.”

12. EQUITY ACTS IN PERSONAM.

In personam is a Latin phrase meaning “directed toward a particular person”

Forex Trading – A Step-by-Step Complete Self-Study eBook by Akonnor Owusu Larbi

1.0 THE FOUNDATION

1.1 INTRODUCTION TO FOREX MARKET

According to the Bank of International Settlements, foreign exchange trading increased to an average of $5.3 trillion a day. To simply break this down, the average has to be $220 billion per an hour. The foreign exchange market is largely made up of institutional investors, corporates, governments, banks, as well as currency speculators. Roughly 90% of this volume is generated by currency speculators capitalizing on intraday price movements.

Unlike the stock market and future markets that are housed in central physical exchanges, the foreign exchange market is an over0 the counter market, decentralized market completely housed electronically.

Though investors are familiar with the stock market they are unaware how small in volume it is in relation to the Forex Market.

In sum, the forex market size and depth make it the ideal trading market. This liquidity makes it easy for traders to sell and buy currencies. This is the reason why traders from all over the world are turning to the FX Market.

1.0.1 KEY BASIC POINTS

Forex stands for Foreign Exchange market

Forex traders trade international currencies

The Forex market is decentralized. This means that there is no one single Forex market, like in stock trading and local exchanges for example.

The Forex market is the largest financial market in the world

The Forex market is open 24 hours a day, 5 ½ days a week

Currencies are always traded in pairs

You can buy and you can sell currency pairs

1.0.1 Advantages of Trading the Forex Market

There are many benefits and advantages of trading forex. Below is a few reasons why so many people are choosing this market:

1. No commissions

No clearing fees, no exchange fees, no government fees, no brokerage fees. Most retail brokers are compensated for their services through something called the “bid/ask spread”.

2. No middlemen

Spot currency trading eliminates the middlemen and allows you to trade directly with the market responsible for the pricing on a particular currency pair.

3. No fixed lot size

In the futures markets, lot or contract sizes are determined by the exchanges. A standard size contract for silver futures is 5,000 ounces.

In spot forex, you determine your own lot, or position size. This allows traders to participate with accounts as small as $25 to $50.

4. Low transaction costs

The retail transaction cost (the bid/ask spread) is typically less than 0.1% under normal market conditions. For larger transactions, the spread could be as low as 0.07%. Of course, this depends on your leverage and all will be explained later in this trading course with Akonnor Owusu Larbi.

5. A 24-hour market

There is no waiting for the opening bell. From the Sunday evening 8:30 PM GMT to Friday Evening 9:00 PM GMT, the forex market never sleeps. This is awesome for those who want to trade on a part-time basis because you can choose when you want to trade: morning, noon, night, during breakfast, or in your sleep.

6. No one single person can manipulate the Market

The foreign exchange market is so huge and has so many participants that no single entity (not even a central banks of US and JAPAN) can control the market price for an extended period of time. This being said, Fundamentals do play a role in volatility. Fundamentals will be explained later.

7. Leverage

In forex trading, a small deposit can control a much larger total contract value. Leverage gives the trader the ability to make nice profits, and at the same time keep risk capital to a minimum. For example, a forex broker may offer 50-to-1 leverage, which means that a

$50 dollar margin deposit would enable a trader to buy or sell $2,500 worth of currencies. Similarly, with $500 dollars, one could trade with $25,000 dollars and so on. While this is all gravy, let’s remember that leverage is a double-edged sword. Without proper risk management, this high degree of leverage can lead to large losses as well as gains.

8. High Liquidity

Because the forex market is very large in size, it is also extremely liquid. This is an advantage because it means that under normal market conditions, with a click of a mouse you can instantaneously buy and sell at will as there will usually be someone in the market willing to take the other side of your trade. You are never “stuck” in a trade. You can even set your online trading platform to automatically close your position once your desired profit level (a limit order) has been reached, and/or close a trade if a trade is going against you (a stop loss order).

9. Low Barriers to Entry

You would think that getting started as a currency trader would cost a ton of money. The fact is, when compared to trading stocks, options or futures, it doesn’t. Online forex brokers offer “mini” and “micro” trading accounts, some with a minimum account deposit of $25. We’re not saying you should open an account with the bare minimum, but it does make forex trading much more accessible to the average individual who doesn’t have a lot of start-up trading capital.

10. Demo Platforms

Most online forex brokers offer “demo” accounts to practice trading and build your skills, along with real-time forex news and charting services. These services are all free. Demo accounts are very valuable resources for those who are “financially hampered” and would like to hone their trading skills with “play money” before opening a live trading account and risking real money.

1.2 A Forex Pair

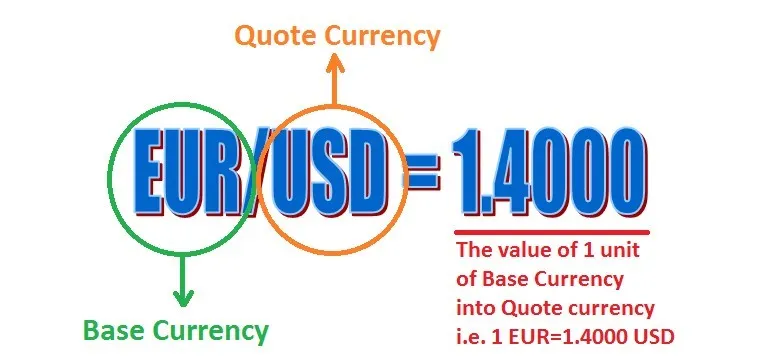

Currencies are always traded in pairs. This means Currencies are traded like AAA/BBB .In simple terms, one can buy and sell currency pairs.

The first currency in a currency pair is the base currency and the second one is the quote currency.

If there is a pair say, EUR/USD, you buy the base currency and sell the quote currency.

Every Forex pair has 2 prices:

1 — Ask price: The price sellers are willing to sell — The price you pay when you enter a buy trade

2 — Bid price: The price buyers are willing to pay — The price you pay when you enter a sell trade

The difference between the bid and the ask price is called the spread which is a cost of trading.

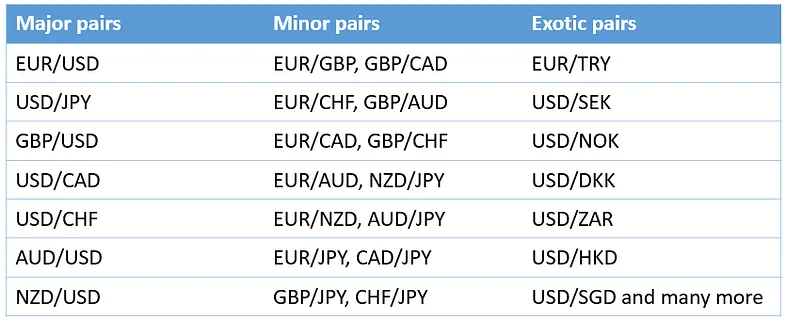

There are 3 different classes when it comes to Forex pairs: Majors (the most commonly traded),Minors and Exotic Forex pairs.

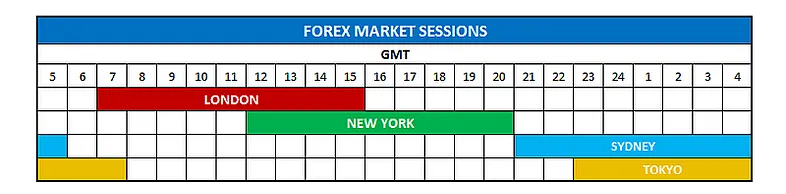

Individual currencies are most active during their own “trading session”

The table below shows the global Forex trading sessions. When the trading sessions overlap, you usually have the highest trading activity. The time is in Greenwich Mean Time. GMT is the mean solar time at the Royal Observatory in Greenwich, London, reckoned from midnight.

1.0.1 Turnover of Currency Pairs

1.1 TRADING PLATFORM

A trading platform is software through which investors and traders can open, close, and manage market positions through a financial intermediary. Online trading platforms are frequently offered by brokers either for free or at a discount rate in exchange for maintaining a funded account and/or making a specified number of trades per month.

Often times, trading platforms will come bundled with other features, such as real-time quotes, charting tools, news feeds, and even premium research. Platforms may also be specifically tailored to specific markets, such as stocks, currencies, options, or futures markets.

Trading platforms may have specific requirements to qualify to use them. For example, day trading platforms may require that traders have at least $25,000 in equity in their accounts and be approved for margin trading, while options platforms may require approval to trade various types of options before being able to use the trading platform.

They are many Trading platforms. These include:

MetaTrader 5— MetaTrader 5 is a platform for trading Forex, analyzing financial markets and using Expert Advisors. Mobile trading, Trading Signals and the Market are the integral parts of MetaTrader 5 that enhance your Forex trading experience.

Interactive Brokers — Interactive Brokers is the most popular trading platform for professionals with low fees and access to markets around the world.

TradeStation — TradeStation is a popular trading platform for algorithmic traders that prefer to execute trading strategies using automated scripts developed with Easy Language.

TDAmeritrade — TDAmeritrade is a popular broker for both traders and investors, especially following its acquisition of ThinkorSwim and the development of the Trade Architect platforms.

1.0.1 Understanding Metatrader 5 (MT4 older Version)

Metatrader 5(MT5) is the most popular trading platform among retail traders. It is simple enough for beginners to start trading with MT4 or MT5, as their first platform, but its advanced functionalities (such as dozens of built-in indicators, graphical tools, the ability to run trading robots, EAs) make it perfect for intermediate or even advanced traders.

7 Easy Steps

1. Download MetaTrader 5/MT5. The first step is to get MetaTrader 5 downloaded onto your computer or laptop or mobile phone. …

2. Follow your Computer’s Prompt. …

3. Tick the License Agreement Box. …

4. Click Finish..…

5. Open an Account. …

6. Input your Details. …

7. Save your Login and Password.

1.0.1 How to open and configure a chart in MT4 or MT5?

After installing Metatrader5 on your computer or mobile phone, the graphics in the terminal are displayed in a standard way. But all traders visually absorb information in different ways, that’s why MT5 provides the ability to change the options of charts to display them in accordance to your desires.

Standard settings are not suitable for analyzing the price movements for many traders, so if you want to change something, you can reorganize the scale, period, and the color of charts. In general, MT5 provides many functions for modifying graphs, and below I will tell about it in details.

1.0.1 Opening of the new graphics

To open a new chart in MT5, you can use one of the next ways:

1. Open the window “market watch”, click the right mouse button on the desired currency pair and choose the menu item “Chart Window”.

2. On the toolbar, click the + button , then select a group of trading instruments from the drop down list.

1. Follow the path: “Window” — “New window”, then repeat step 2.

2. Follow the path: “File” — “New schedule”, then repeat step 2.

Please note: only characters opened in the window “market watch” will be displayed in the list of trading instruments.

To display all symbols, press the right mouse button on any field of the window “market watch” and click on the row “Show all symbols”.

1.0.2 Zoom

The scale of the graph plays an important role in the observation of price movements. Zoom allows you to focus on the details while reducing the figure gives an opportunity to look at the General trend.

In MT4, you can use several ways to change the chart scale:

2. Go to the “Charts” in the main menu bar — “Increase” / “Decrease”;

3. Hold down the Shift + / — (“plus” or “minus”);

4. On the toolbar ;

5. Anywhere in the active window open the context menu by pressing the right mouse button and then refer to the command “Increase” or “Decrease”.

1.0.1 Changing time frames

if you need to determine the exact point to enter the market, You should choose a narrow time frame for plotting. However, for assessing the General trend you need a wide timeframe. When you have built the graphic, you can change time periods in the following ways:

· Go to the tool bar “chart Period”, which includes all possible time frames;

· On the toolbar the “Charts” click on the button

· In the active chart window of the shortcut menu invoked by the right mouse button, select “Period”;

· Follow the path: “Graphics” in the main menu bar — “Period”.

1.0.2 Changing the type of chart display

MT5 offers traders to switch between different chart types easily. Clicking on “Graphics” in the main menu bar you can choose the visualization of the line chart, bar chart, and the Japanese candlestick chart. The same function is available in the toolbarL: just click on the corresponding icon. You can also use Alt+1, Alt+2, and Alt+3

1.0.3 Color changing graphics

On MT5, a trader can change the chart color for his own convenience by clicking on the trend line in the popup menu chooses “Properties”. In the next window, you can define the color of each element of your schedule in the tab “Colors”.

On the terminal, three color versions are set automatically for graphics. In the “Color scheme”, you can select the yellow graphics on a black background, it is also possible to choose green on a black background, and for conservative traders there is a black-and-white palette. In addition to autocomplete in the right box you can choose the color of each element separately

1.0.1 Saving graph settings on the terminal with templates

MT4 has a built-in ability to save and then select a previously configured graph. This eliminates the need to adjust every time the visualization window. With one click You can apply a favorite solution that will allow You to analyze the price movement quickly. MetaТrader allows you to save these properties:

· color scheme;

· timeframe (period of time);

· indicators with all the settings;

· graphic tools (in this case, price values are also saved on the new graph and you will have to adjust);

· chart scale;

· the type of graph;

· attached the TA and all its settings.

In order to save all settings in the database, just press the save button on the toolbar, then select “Save template”

A similar option is available under “Graphics” in the main menu bar — “Template” — “Save template” or in the context menu of the graph.

For activating a saved template, click on the button

, then on “Load template”. Once you find the desired version of the template, click “Open” and the graph will be shown in the right

way. You can remove a template by a similar way, choosing the line “Remove template”.

With all these, you can equally trade on your mobile phone by downloading MT5 from Play Store or The App Store.

1.4 THE TRADING ORDER TYPES

Here are the basic trading order types:

1.4.1 Market Order

A Market order is the simplest order type. There are market orders to buy and market orders to sell. A market order gives you whatever price is available in the marketplace.

1.4.2 Buy Limit Order

A Buy Limit is an order to buy that is placed below the current price. The order is only filled* at or below the limit price.

1.4.3 Sell Limit Order

A Sell Limit is an order to sell (or short) that is placed above the current price. The order is only filled at or above the limit price.

1.4.4 Buy Stop Order

A Buy Stop is an order to buy that is placed above the current price. The order is only filled at or above the stop price.

1.4.5 Sell Stop Order

A Sell Stop order is an order to sell that is placed below the current price. The order will only be filled at or below the stop price.

1.4.6 Buy Stop Limit

A Buy Stop Limit order is very similar to a Buy Stop order, except that it doesn’t act like a market order. The buy stop limit will only fill at the buy stop limit price or lower.

1.4.7 Sell Stop Limit

A Sell Stop Limit Order is very similar to a Sell Stop order, except that it doesn’t act like a market order. The sell stop limit will only fill at the price equivalent to the limit price attached to the order, or higher.

Getting used to all the trading orders can be a bit confusing at first, and there are more order types than this!. Putting out the wrong order type when money is on the line can cause big problems.

2.0 THE BASICS

2.0.1 CURRENCY VALUE

The value of a currency pair Is determined by the strength or weakness of the base currency in relation to the quote currency. The base currency is almost 1 for most currencies. This means that, when you see a quote of 1.4567 EURUSD, its value is 1 EUR will buy 1.4567 of USD. If you sell EURUSD from 1.4567 to 1.4557, you would have made a profit of 10 pips.

2.0.2 WHAT IS A PIP?

PIP stands for Price Interest Points. There is Standard lot ($100,000), Mini Lot ($10,000) and Micro lot ($1000). In the standard lot, a pip worth $10. Mini lot its $1 and its worth $0.1 in micro lots. However, each currency has its own pip value.

2.0.3 PIP VALUE

The table below shows the value of a pip in each currency Pair. Remember, currencies are traded in pairs.

These values changes slightly based on the actual exchange rates, but the fluctuations are very minor.

2.0.4 AVERAGE DAILY PIPS

Getting to know the average daily pips movement is crucial in calculating profit and loss. It helps in entry price levels and getting out of the market as early as possible. The table below shows the six (6) major pairs and their average pips pulled per day.

2.0.5 TURNOVER OF THE SIX MAJOR PAIRS

Turnover is an aggregated cost of all trading deals in as specified time period. In technical analysis, the turnover measures efficiency and intensity of assets allocation. In simple terms, the turnover is the total volume of all transactions in a given time period.

2.0.6 THE US-INDEX

The U.S. Dollar Index (USDX, DXY, DX) is an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies. The Index goes up when the U.S. dollar gains “strength” (value) when compared to other currencies. Pay close attention to the US-Index. The US- Index sets the tone for a lot of currency moves. It can help you price analysis and trade timing in the forex market.

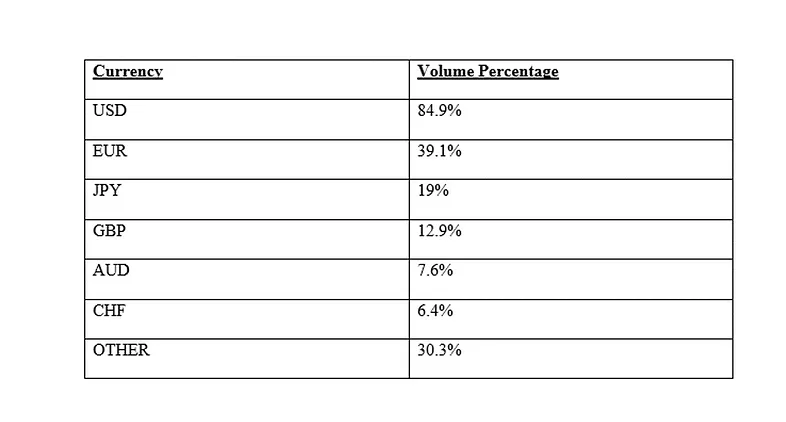

It is a weighted measure using the dollar’s movements relative to other select currencies in an attempt to represent major trading partners. The current mix is approximately:

· 57.6% Euro (EUR)

· 13.6% Japanese Yen (JPY)

· 9.1% Canadian Dollar (CAD)

· 4.2% Swedish Krona (SEK)

· 3.6% Swiss Franc (CHF)

The basket was altered in 1999 when the Euro replaced several European currencies. It still includes the Swedish krona and the Swiss franc despite the fact that China, Mexico, and South Korea are more important trading partners.

2.0.7 GLOBAL TRADING SESSIONS AND WHEN PAIRS MOVES

Although the forex market is open 24 hours, 5 ½ days, it is however important to keep track of the individual trading sessions as they Impact FX rates and volatility significantly.

It is vital to understand that a currency moves most when their local market is open. The most active trading session is when London and New York overlap, thus from 12:00 to 15:00 GMT each trading day.

2.0.8 THE IMPORATNCE OF CLOBAL TRADING SESSIONS

The trading session impacts multiple trading decisions on multiple levels. These include:

1. Market Selection

Choose a pair that is most active when you are infront of your charts. Choosing a pair that is not active during your trading can suck you in low volatility and boring price moves.

1. Good Entries and Exist

Before entering a trade, make sure to analyse price in context to the current trading session and then make your decisions accordingly.

2. Breakouts during active session

A Breakout that occurs during a pair’s actual trading session is much more likely to succeed. For example, a breakout move in USDCAD that happens during US trading sessions is more likely to succeed.

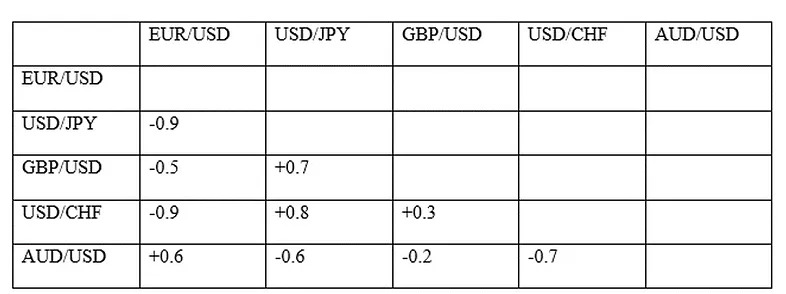

2.0.9 FOREX RATES CORRELATION & RISK IN TRADING

For risk management sake, apply the strongest position and negative correlations; +1 or _1 or –

!00%. A positive correlation means the market will move in the same direction. A negative correlation means it will move in opposite direction.

2.1.0 RISK MANAGEMENT

It is important to know that, trading moving currency pairs with a high positive correlation, you are increasing your risk as both pairs are moving in same direction. This means, there is likelihood of either having 2 winning or 2 loses at the same time.

2.1.1 LEVERAGE

Leverage is an investment strategy of using borrowed to increase the potential returns of an investment. Leverage allows you to enter a position or trade that is larger than your capital.

Leverage in Forex can be in the forms 1:100

1:200

1:300

1:400

1:500

For instance, a leverage of 1:100 means if you have $10,000, you can control an account size of

$ 1,000,000. The higher the leverage, the higher the win and vice versa.

2.1.0 SPREAD

Spread is the difference between the bid and ask. It represents brokerage service costs and replaces transactions fees. Spread is traditionally denoted in pips — a percentage in point, meaning fourth decimal place in currency quotation.

Types of Spreads in Forex

Fixed spread — difference between ASK and BID is kept constant and do not depend on market conditions. Fixed spreads are set by dealing companies for automatically traded accounts.

Fixed spread with an extension — certain part of a spread is predetermined and another part may be adjusted by a dealer according to market.

Variable spread — fluctuates in correlation with market conditions. Generally variable spread is low during times of market inactivity (approximately 1–2 pips), but during volatile market can actually widen to as much as 40–50 pips. This type of spread is closer to real market but brings higher uncertainty to trade and makes creation of effective strategy more difficult.

A trader needs to cover spreads in winning trades before making a profit. For example, let’s take EUR/USD, the price of 1.4652 which is the bid and 1.4650 which is the ask price. This means that the spread charge is 2 pips. Therefore, in the case of selling USD, if price moves to 1.4552,

there is a successful pull of 100 pips. However, a spread of 2 pips will be deducted, making the investor basket 98 pips.

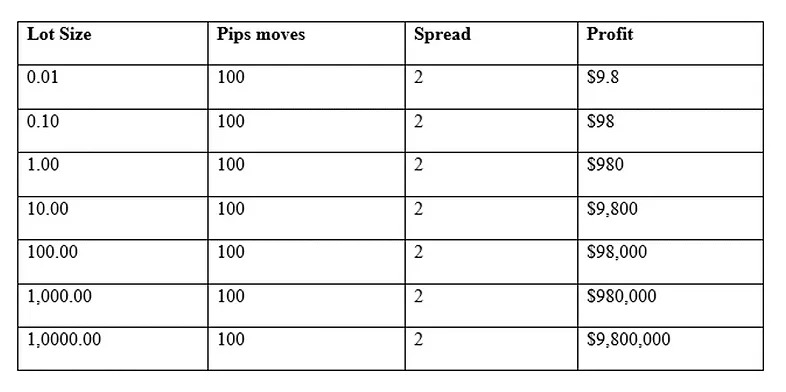

2.1.2 LOT SIZE

The pip value depends on the lot size you enter a trade with. Lets take the EURUSD example again. At the price of 1.4652 and leverage of 1;100, if an investor sell with lot size of 0.01, when it moved to 1.4552, the 98pips would produce $9.8.

The table below shows how much profit can be made with different lot sizes.

2.1.2 Calculating Pip Value

Trading EURUSD, with account in USD, one pip = 0.001 Let say your trade accounts is $10,000

0.001*10,000 =10

If the exchange rate is 1.13798 10/1.13798=8.7875007

Therefore a pip of EURUSD @ a value of 1.13798 worth $8.79 For metal, you calculate thick value instead of pip value.

Rick value=tick in decimal(0.01) *number of trading lot of 100oz

=0.01*100

=1

Each tick is worth $1.

Modules & Content Structure to follow

Below you find some of the modules that await you.

You can equally join over 500,000 people benefiting from my articles.

1. Setting up trading charts

2. Introduction to trading principles

3. Chart reading foundation

4. Getting to know your trading tools

5. Signal introduction

6. Step-by-step setup exploration

7. Master all my setups

8. Finding the perfect entries

9. How to set effective stops

10. Defining the best targets

11. How to manage a trade

12. When to cut a losing trade

13. Position sizing

14. Risk management

15. Market selection and trading plans

16. Dealing with news events

In addition, these are the 7 price action you could master when you sign up for our Newsletter

1) Trading with trendlines -Mastering trend structure

2) The best chart patterns

3) Drawing support and resistance the right way

4) How to use the Fibonacci tool

5) The Pinbar trading signal

6) Clean vs messy charts

7) Multi timeframe analysis

Thank you for reading. — Akonnor Owusu Larbi